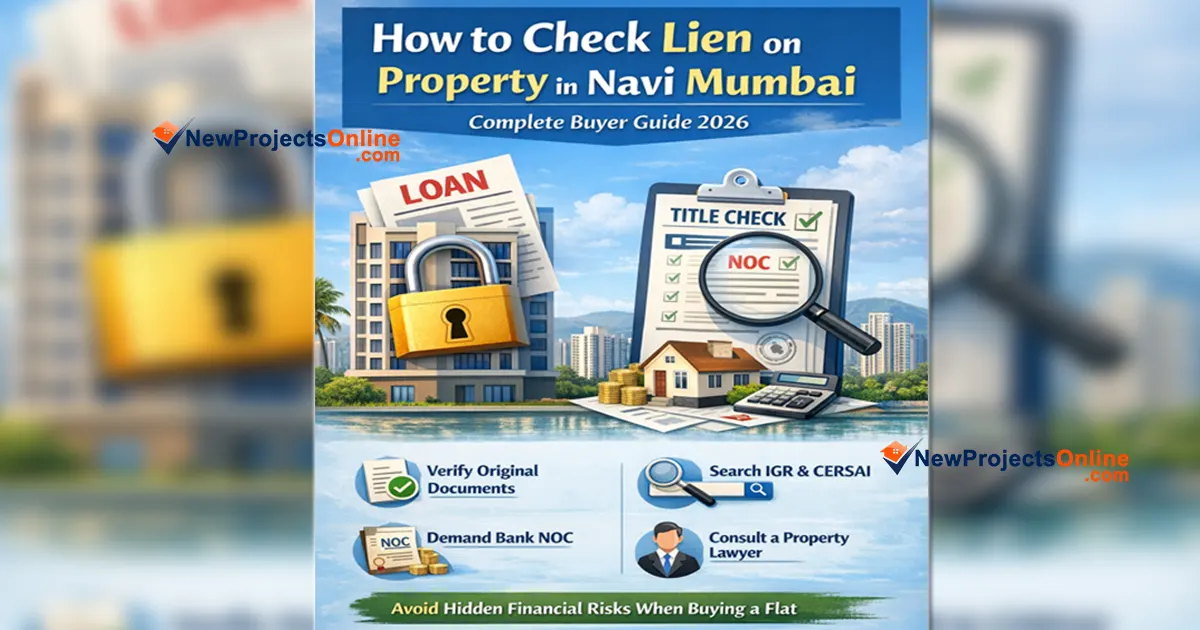

How to Check Lien on Property in Navi Mumbai (Complete Buyer Guide 2026)

Buying a flat in Navi Mumbai is one of the biggest financial decisions most people make. But before you finalize any deal, there is one critical question you must answer:

Is this property completely free from any lien, loan, or financial claim?

A property may look perfect on the surface — occupied, maintained, and legally owned — yet still be tied to a bank, lender, or authority. This is where most buyers make costly mistakes.

This guide explains how to check lien on property in Navi Mumbai in a practical, real-world way — so you can avoid hidden risks and buy with confidence.

What Does “Lien on Property” Mean in Navi Mumbai?

A lien simply means that someone else has a legal or financial claim on the property.

In most cases, this happens when:

- The owner has taken a home loan

- The property is used as security for a loan

- There are unpaid dues (society, tax, or authority)

Important: A person can still live in the flat and be the legal owner — but cannot freely sell it until the claim is cleared.

Quick Reality Check for Buyers

| Common Assumption | Reality |

|---|---|

| Seller is living there → property is clear | ❌ Not always true |

| Society papers are clean → no loan | ❌ Not enough proof |

| Bank loan = problem | ❌ Can be handled safely if structured properly |

| Only legal disputes matter | ❌ Financial claims matter equally |

Why This Matters More in Navi Mumbai

Navi Mumbai has a unique property ecosystem. Many properties involve:

- CIDCO leasehold history

- Co-operative housing societies

- Resale flats with past loans

- Under-construction projects with builder finance

This means multiple layers of financial and legal checks are required before buying.

Step-by-Step: How to Check Lien on Property

1. Ask Directly About Loan Status

Start simple. Ask the seller clearly:

- Is there any active home loan?

- Is the property mortgaged?

- Has any loan been recently closed?

Tip: Always ask for written confirmation later in the agreement.

2. Verify Original Property Documents

This is the most important step.

- Ask to see original sale deed

- Check complete chain of ownership

- If originals are not available → assume bank involvement

Red Flag: “Documents are with bank” without proof.

3. Check IGR Maharashtra Records

You can search property registration details through:

- Index II (free search)

- E-search for registered documents

This helps you identify:

- Past sale transactions

- Registered mortgage documents

- Ownership history

Important: A clean search is good — but not final proof.

4. Search CERSAI (Loan / Mortgage Check)

CERSAI is a central registry where banks record property-backed loans.

- Search using property details

- Look for registered security interest

This helps detect hidden or active loans.

5. Ask for Loan Closure Proof

If a loan existed, demand:

- No Dues Certificate

- Loan Closure Letter

- Bank NOC (No Objection Certificate)

- Proof of document release

Without these → do not proceed.

6. Verify Society & Local Dues

- Society maintenance dues

- Property tax

- Water / electricity dues

These may not be “lien” technically — but they can block transfer.

7. Check MahaRERA (For New Projects)

For under-construction properties:

- Check project registration on MahaRERA

- Review encumbrance disclosures

- Check builder financial status

This helps identify project-level financial risks.

Common Red Flags You Should Never Ignore

- Seller refuses to show original documents

- Pressure for quick token payment

- Unusually low price

- Loan “almost closed” but no proof

- Payment requested to personal account instead of bank settlement

- Incomplete document chain

Golden Rule: One red flag = caution. Multiple = walk away.

Can You Buy a Property with Existing Loan?

Yes — but only if handled properly.

Safe structure usually includes:

- Loan outstanding clearly defined

- Payment routed to bank first

- Bank issues NOC and releases documents

Never rely on verbal promises.

Who Should Verify What?

- Buyer: Ask questions, check documents

- Bank: Protects its loan, not your risk

- Broker: Facilitates deal, not legally responsible

- Society: Confirms dues, not loan status

- Advocate: Protects your ownership

Always involve a property lawyer.

Final Checklist Before Registration

- Original documents ready for transfer

- Loan closure proof available

- Bank NOC obtained

- Society dues cleared

- Property tax cleared

- Agreement reviewed by advocate

Conclusion

A lien is not just a legal term — it is a real financial risk that can delay, block, or damage your property purchase.

The safest buyers follow a simple strategy:

- Verify everything

- Trust documents, not words

- Use multiple checks (IGR, CERSAI, MahaRERA)

- Always involve a legal expert

A flat is only truly yours when it is legally and financially clear.

FAQs

Is lien the same as home loan?

No. A home loan is the debt. A lien is the legal claim created because of that debt.

Can I buy a flat with an existing loan?

Yes, if the loan is properly cleared during the transaction with full documentation.

Do society papers prove property is clear?

No. They only confirm society-related dues and membership status.

Is MahaRERA enough for verification?

No. It helps for project-level details but does not replace legal due diligence.

Is lawyer verification necessary?

Yes. It is one of the most important steps in property buying.

Save • Share • Help someone avoid a costly mistake

Popular Property Searches

Explore Top Cities

Property Status

Ready To Move Flats in Navi Mumbai Ready To Move Flats in Mumbai Ready To Move Flats in Raigad Ready To Move Flats in Dombivli Under Construction Flats in Navi Mumbai Under Construction Flats in Mumbai Under Construction Flats in Thane Under Construction Flats in Kalyan Under Construction Flats in Pune Under Construction Flats in DombivliExplore More Real Estate Insights

Discover more valuable content to help with your property journey: